Mutual funds sahi hai! But which one?

Investing in equity is unarguably one of the best, if not the best, investment options available to the long-term investors. If the economy has to grow, businesses in the country have to flourish; and if businesses flourish, so will the market price of these businesses and the investors’ wealth. Also, investing through mutual funds (MF) is the only sensible way to invest in equity for the majority of investors as against stock-picking. In the last couple of years a large number of Indian investors have realised this fact which is reflected in the steadily rising amounts being managed by the MF schemes. However, countless retail investors are observed confused about finding the best MF schemes for them. The misleading advertisements and mis-selling by the distributors make the matter worse. This article is an attempt to inform the readers about which MF is right for the purpose of long-term wealth creation while minimising the risks.

To outline briefly, there are two types of equity MFs: Active MFs, and Passive MFs. In Active MFs fund managers try to pick the best stocks to achieve the best possible returns for the investors. He buys the stocks that he thinks will increase in price and sells the ones he thinks are likely to be duds. In Passive MFs (index funds) there is no one selecting the stocks. The fund buys all the stocks that comprise an index. The most popular indexes in India are Bombay Stock Exchange’s SENSEX (comprising of 30 largest companies) and National Stock Exchange’s NIFTY (comprising of 50 largest companies). A SENSEX-tracking index fund will buy and hold shares of all of the 30 largest companies in India while the NIFTY-tracking index fund will buy and hold shares of all of the 50 biggest companies in India. (In this article, by ‘index fund’ I refer to the traditional and most common equity index funds that invest in stocks of a popular equity indexes in the proportion of their market capitalisations.)

As per the data of AMFI, Indian investors are investing predominantly in the active MFs. However, active MFs are highly inefficient, and therefore, index funds are clearly a better choice!

Add to this fact the costs associated with managing the funds. After accounting for the costs, all the investors together would have definitely earned less than 12%, in the year in which the market has yielded 12%. The difference between the return provided by the market and the total return earned by the investors will be exactly equal to all the investment costs put together. If all the costs amount to 2.5% of the total amount under management, all the investors put together would earn 9.5%, when the market yielded 12%.

If you don’t realise how big a difference this makes, consider this: A Rupee invested today would become Rs. 30 in 30 years if annual return of 12% is achieved. However, at investment costs of 2.5% per annum, the corpus at the end of 30th year would be halved to Rs. 15! Compounding works wonders when it works for you; but destroys wealth when it works against you.

It should not be surprising to know that most active MFs earn significantly less than what the total market yields in the long run. I do not question the abilities of the fund managers. Generally, they are smart, well-educated and knowledgeable people. But they are competing with one another. When one buys a stock, another sells it, while there is no net gain to the investors as a group. In fact the investors incur loss exactly equal to the fees they pay to these intermediaries. Successful investing, then, is about minimising the share of the returns earned by the businesses that is consumed by Dalal-Street and maximizing share of the returns earned by you.

The probability of your active MF scheme beating the index returns, after all the costs, is extremely slim. On the other hand, the costs associated with index funds are remarkably low, and therefore, they provide you almost all the returns the total market yields. Unsurprisingly, they perform much better in the long run. By a wide margin.

Management fees and operating expenses (expressed as Total Expense Ratio):They include fees of the team that manage the fund, rent of their office and other operational & administrative expenses. If you invest directly with the MF company, the expense ratio in Active MF schemes is generally in the range of 1%-1.5%. If you invest in ‘regular plans’ through a distributor/broker, the expense ratio is normally in the range of 2%-2.5%. In index funds purchased directly through MF companies the expense ratio is in the range of 0.1%-0.25% in India which may reduce further as size of these index funds increase. The MF companies are mandated to declare the expense ratios of their MF schemes regularly.

Hidden costs of portfolio turnover: The active MFs buy and sell stocks. In doing so they incur costs such as brokerage commissions, taxes, bid-ask spreads, etc. The more the fund manager trades, the higher are the costs. These costs are more pernicious in nature as they are not reflected in the expense ratio, and therefore, are ignored by the investors. These costs are difficult to measure but we can assume them to be in the range of 0.5%-1% depending on the turnover for a given active MF. The beauty the index fund is that it never needs to be rebalanced by buying and selling shares (except when a stock is added to or removed from the index), and therefore, do not incur the costs pertaining to portfolio turnover.

All these costs amount to at least 2-3% for active MFs as against that of around 0.5% or less for index funds. We have seen how much wealth destruction can be caused by the impact of such costs compounding over a long-term.

If you put together the two facts in front of you that (i) beating the market is a zero-sum-game before costs and (ii) the cost of managing money by active MFs is staggering, you realise how improbable it is for an active MF to beat the index (market-returns) over the long term.

To outline briefly, there are two types of equity MFs: Active MFs, and Passive MFs. In Active MFs fund managers try to pick the best stocks to achieve the best possible returns for the investors. He buys the stocks that he thinks will increase in price and sells the ones he thinks are likely to be duds. In Passive MFs (index funds) there is no one selecting the stocks. The fund buys all the stocks that comprise an index. The most popular indexes in India are Bombay Stock Exchange’s SENSEX (comprising of 30 largest companies) and National Stock Exchange’s NIFTY (comprising of 50 largest companies). A SENSEX-tracking index fund will buy and hold shares of all of the 30 largest companies in India while the NIFTY-tracking index fund will buy and hold shares of all of the 50 biggest companies in India. (In this article, by ‘index fund’ I refer to the traditional and most common equity index funds that invest in stocks of a popular equity indexes in the proportion of their market capitalisations.)

As per the data of AMFI, Indian investors are investing predominantly in the active MFs. However, active MFs are highly inefficient, and therefore, index funds are clearly a better choice!

Why Index MFs are a better investment option than Active MFs?

The index funds are likely to perform much better than active MFs in the long run because of these two reasons: (1) beating the market is a zero-sum-game before costs and negative-sum-game after costs, and (2) The costs associated with active MFs are enormous. I will elaborate on both of these points below.(1) Beating the market is a negative-sum-game

The fundamental truth that the MF industry does not want you to understand is that investing in equity is a zero-sum-game at market-returns. Suppose all the stocks in the market, in totality, provide a return of 12% in a given year. In this given year, for every rupee that has earned a return of 13% (1% above its share of 12%), there has to be another rupee that has earned a return of 11% (1% below its share of 12%). Clearly, all the investors together would definitely have earned 12%. Not a penny more, not a penny less. This is basic arithmetic. If you want to sound smart, say that against every alpha there has to be a negative alpha.Add to this fact the costs associated with managing the funds. After accounting for the costs, all the investors together would have definitely earned less than 12%, in the year in which the market has yielded 12%. The difference between the return provided by the market and the total return earned by the investors will be exactly equal to all the investment costs put together. If all the costs amount to 2.5% of the total amount under management, all the investors put together would earn 9.5%, when the market yielded 12%.

If you don’t realise how big a difference this makes, consider this: A Rupee invested today would become Rs. 30 in 30 years if annual return of 12% is achieved. However, at investment costs of 2.5% per annum, the corpus at the end of 30th year would be halved to Rs. 15! Compounding works wonders when it works for you; but destroys wealth when it works against you.

It should not be surprising to know that most active MFs earn significantly less than what the total market yields in the long run. I do not question the abilities of the fund managers. Generally, they are smart, well-educated and knowledgeable people. But they are competing with one another. When one buys a stock, another sells it, while there is no net gain to the investors as a group. In fact the investors incur loss exactly equal to the fees they pay to these intermediaries. Successful investing, then, is about minimising the share of the returns earned by the businesses that is consumed by Dalal-Street and maximizing share of the returns earned by you.

The probability of your active MF scheme beating the index returns, after all the costs, is extremely slim. On the other hand, the costs associated with index funds are remarkably low, and therefore, they provide you almost all the returns the total market yields. Unsurprisingly, they perform much better in the long run. By a wide margin.

(2) Costs associated with active MFs are enormous

There are mainly following costs that MF investors pay to the intermediaries:Management fees and operating expenses (expressed as Total Expense Ratio):They include fees of the team that manage the fund, rent of their office and other operational & administrative expenses. If you invest directly with the MF company, the expense ratio in Active MF schemes is generally in the range of 1%-1.5%. If you invest in ‘regular plans’ through a distributor/broker, the expense ratio is normally in the range of 2%-2.5%. In index funds purchased directly through MF companies the expense ratio is in the range of 0.1%-0.25% in India which may reduce further as size of these index funds increase. The MF companies are mandated to declare the expense ratios of their MF schemes regularly.

Hidden costs of portfolio turnover: The active MFs buy and sell stocks. In doing so they incur costs such as brokerage commissions, taxes, bid-ask spreads, etc. The more the fund manager trades, the higher are the costs. These costs are more pernicious in nature as they are not reflected in the expense ratio, and therefore, are ignored by the investors. These costs are difficult to measure but we can assume them to be in the range of 0.5%-1% depending on the turnover for a given active MF. The beauty the index fund is that it never needs to be rebalanced by buying and selling shares (except when a stock is added to or removed from the index), and therefore, do not incur the costs pertaining to portfolio turnover.

All these costs amount to at least 2-3% for active MFs as against that of around 0.5% or less for index funds. We have seen how much wealth destruction can be caused by the impact of such costs compounding over a long-term.

If you put together the two facts in front of you that (i) beating the market is a zero-sum-game before costs and (ii) the cost of managing money by active MFs is staggering, you realise how improbable it is for an active MF to beat the index (market-returns) over the long term.

The fallacy of past track-record

Survivorship bias

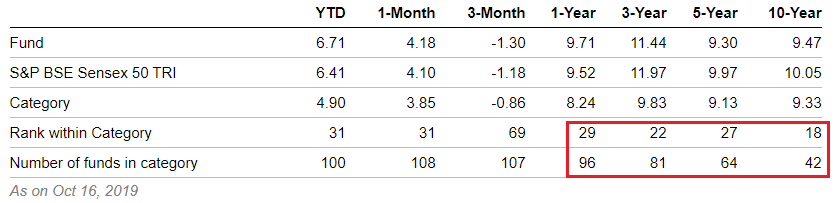

The reader must wonder that despite the reasons mentioned above why so many MF schemes have a past track-record of beating the index. To find the truth, consider the comparison of return provided by a typical index fund with the returns provided by other MFs in the same category.

The index fund has ranked 18th out of 42 when 10 years' performance is compared. Similarly, it has ranked 27th out of 64 for 5 years, 22nd out of 81 for 3 years and 29th out of 96 for 1 year. The performance clearly appears to be better than average, but is still nothing close to what can be called outstanding in comparison to the active MFs. However, you must have noticed that as tenure increases, the number of funds in the category reduces. One of the major reasons for the same is that a lot of MF schemes do not survive in the long run (mainly due to their inability to beat the index). These schemes were either discontinued or were merged with other schemes. The total schemes active before 10 years must be many more but only 42 have survived until today. Out of those 42 that have survived, the index fund has ranked 18th. As more years pass, even lesser schemes would survive and outperform the index fund. When we see many presently available MF schemes that have outperformed the index, a strong survivorship bias is misleading us. The investor must recognize the fact that an average MF can never outperform the market - it is not possible arithmetically.

No correlation between past and future performances

What if you identify the fund that has consistently outperformed the index in the past, and choose the same for your investment?

MFs have comparatively short history in India. However, in the long history of MF in the USA, studies have proven that the past performance has proved to be of no significance to find out which MF schemes would perform better in the future. Reversion to Mean, rather than the average of past performance, has proven to be a strong force as far as performance of MFs are concerned. When the MF scheme document disclaimer mentions that “Past performance is not indicative of future returns”, the investors better pay attention!

There can be many reasons for outperforming the index being unsustainable for longer durations: The fund managers and their teams change; increasing fund-size makes outperforming the market more difficult; the investment philosophy that works better during some years do not work in the other; the earlier outperformance was more a matter of chance rather than skill; etc. Whatever the reasons, the indisputable fact is that the fund managers have not been able to continue to outperform the index for long-term.

In short, there is no systematic way to identify the rare MFs, if any, that will outperform the market-returns in the future.

Why does nobody tell you about the superiority of the index funds?

Simply because the MF companies and distributors earn tiny fees in index funds. It is not in their own benefit to suggest you to invest in index fund. There is a clear conflict of interest between the investors and their advisors & managers in most cases.

Also, many advisors and managers actually believe that the MFs suggested/managed by them will outperform the index. John Bogle said paraphrasing Upton Sinclair: “It’s amazing how difficult it is for a man to understand something if he is paid a small fortune not to understand it.”

Shortcomings of index investing

People find it boring. It does not earn the investor any bragging rights. You can’t boast at a dinner party about earning higher returns than everyone else just by accepting the market-returns. But the investor must remember that real investing is not meant to be exciting. The boring regular investments in index funds is purely for the purpose of solid wealth creation in the long run while sparing a lot of time for things you actually love doing!

Apart from that, one genuine limitation for index investing in India is that we don’t have a true broad market index fund. In the USA, there are S&P 500 index funds (covering top 500 companies in terms of their market capitalization) as well as total stock market index funds (covering all the listed companies). These funds provide full benefits of an index fund. In India we have traditional index funds covering Sensex (largest 30 companies), Nifty (largest 50 companies) and Nifty Next 50 (51st to 100th largest companies). In comparison, there are thousands of companies listed on the exchanges. If you invest in the index funds in India, a significant portion of the markets remain untouched by you, which may deprive you of full benefits of investing in a broad market index. An active MF manager having an eye for finding out good smaller companies may outperform such narrow indexes.

Conclusion:

Most active MFs will underperform the corresponding index in the long run. While a tiny number of MF schemes may actually outperform these indices, there is no systematic way to find out today which these MFs will be. So the most sensible investment option for long-term equity investors is Index funds (e.g., ICICI Prudential Nifty Index Fund, Nifty 100 Index Fund, UTI Nifty Index Fund, etc.).

While shortlisting the index funds, the investors should ensure that expense ratio of the fund should be low. Also ensure that significant amount is being managed in the MF scheme you choose to invest in (mentioned as AUM or Assets Under Management); this helps in accurate tracking of the index. The fund manager should also ensure to choose funds of reliable MF companies.

Considering the absence of broad-market index funds in India, the investors may also invest a small portion of their portfolio in multi-cap or mid-cap active MFs after studying these MFs. However, the investor must not build their expectations based on the past track-record of these MFs. Most of these funds may underperform their corresponding indices in the long run. They are also likely to be more volatile and may test the investors' ability to stick with the scheme for long-term.

(If you want to invest in a broader index, some Exchange Traded Funds (ETFs) are presently available in India. ETFs are similar to index funds, the only major difference is that they can be traded in real-time and you need a demat account for owning them. Do ensure that you do not fall into the short-term trading habit if you choose ETFs, as that will make you an active investor, and in that case, you are back to square one!)

So the indisputable right answer to the question, “Konsa Mutual Fund sahi hai?” is “Index funds sahi hai!”

Warren Buffett has always been a strong advocate of the index funds. Here's what he has famously said:

Acknowledgement: John Bogle’s book ‘The Little Book of Common Sense Investing’ played an instrumental role in developing my understanding of index funds. Mr. Bogle was the founder of The Vanguard Mutual Fund Group, which is the second largest MF company in the world. He is credited for contributing the most for the welfare of retail investors by inventing and promoting the concept of index funds.

Warren Buffett has always been a strong advocate of the index funds. Here's what he has famously said:

Acknowledgement: John Bogle’s book ‘The Little Book of Common Sense Investing’ played an instrumental role in developing my understanding of index funds. Mr. Bogle was the founder of The Vanguard Mutual Fund Group, which is the second largest MF company in the world. He is credited for contributing the most for the welfare of retail investors by inventing and promoting the concept of index funds.

Very nice and informative article. Keep doing

ReplyDelete